Meta Platforms (META)

Equity Research

Disclaimer

The analyses and conclusions contained in this report are based on publicly available information. There may be confidential or otherwise nonpublic information in the possession of the companies discussed in this report that could lead these companies and others to disagree with these analyses, conclusions and opinions.

This report may include forward-looking statements, estimates, and projections which reflect various assumptions that may not be accurate.

The content expresses the views of the author as of the time of writing and such views are subject to change. This report and the information contained herein is not investment advice or a recommendation or solicitation to buy or sell any securities. Past performance is not indicative of future results. All investments involve risk, including loss of principal.

Overview

Ticker: META

Stock Price: $598.86

Builds products that connect and share across mobile, PCs, VR headsets, and AI glasses

Founded 2004; IPO 2012

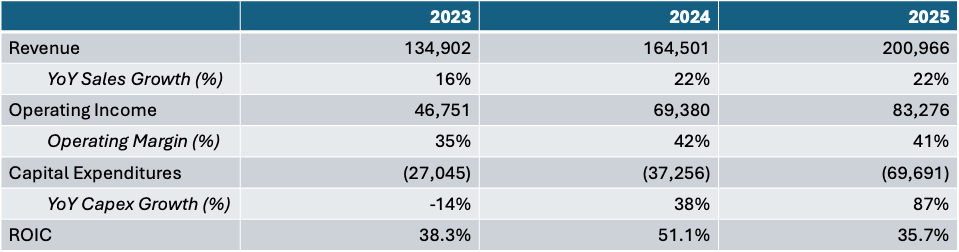

FY2025 revenue of $200.97B (+22% YoY)

Family of Apps 98.9% of revenue ($198.76B); Reality Labs 1.1% ($2.21B)

Advertising $196.18B; other $2.58B

Market capitalization of ~$1.52T

Mark Zuckerberg, founder, chairman, and CEO since 2004 (~22 years)

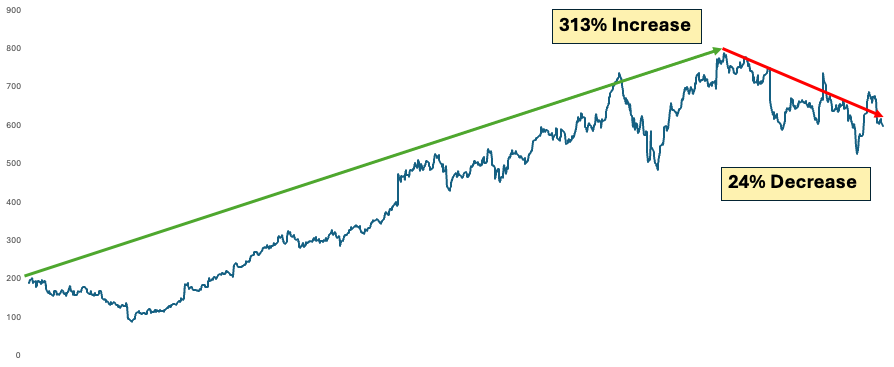

4 Year Stock Performance (since May 2021)

Revenue

Capex has grown 87% YoY – far outpacing revenue growth (22%) but operating margins have fallen by only 1%.

Meta has shown they can still maintain strong operating margins while spending aggressively due to their high ROIC.

FY2025 Revenue Breakdown

By segment (FY2025 revenue: $200.97B)

Family of Apps: $198.76B (98.9%)

Reality Labs: $2.21B (1.1%)

By line item

Advertising: $196.18B

Other: $2.58B

By customer billing geography

US & Canada: $78.87B (39.2%)

Asia-Pacific: $53.82B (26.8%)

Europe: $46.57B (23.2%)

Rest of world: $21.71B (10.8%)

Industry Overview

Digital advertising and social-media attention markets

Smaller, growing exposure to consumer AI and VR/AR hardware and software

Largest scaled players: Alphabet, Amazon, Snap, Pinterest, and ByteDance via TikTok

Peer 2025 advertising scale

Alphabet Google advertising: $294.69B

Amazon advertising services: $68.64B

Snap total revenue: $5.93B; Pinterest total revenue: $4.22B

TikTok: more than 1B monthly users globally; >200M monthly users in Europe

Structural shift

Move beyond 2D screens toward mixed reality and AI; AI-optimized data-center capacity is becoming the key infrastructure layer

Industry Market Dynamics

Rivalry: high

Meta cites direct competition from TikTok and products that appeal to younger users

Large ad budgets also contested by Alphabet and Amazon

Threat of new entrants: low; Buyer power: medium to high

$131.05B of non-cancelable contractual commitments (cloud, servers, networks, data centers, RL hardware) raise barriers

Marketers generally do not have long-term commitments and many spend only a small share of total budgets

Supplier power: medium and rising; Substitute pressure: high

AI infrastructure now requires large purchases of chips, fiber, cloud, power, and construction capacity

Marketing budgets can move among search, retail media, short-form video, streaming, and other channels

Core Product Portfolio

Family of Apps (98.9% of FY2025 revenue)

Facebook, Instagram, Messenger, WhatsApp, and Threads

Q1 2026: 3.56 billion Family daily active people on average for March 2026

Substantially all revenue is generated from advertising on Facebook and Instagram

Reality Labs (1.1% of FY2025 revenue)

VR/AR hardware and software business; remains loss-making but strategically important

Built on the 2014 Oculus acquisition; ships Quest headsets and Ray-Ban Meta smart glasses

AI stack

Meta AI assistant, Llama open-source model family, Muse model family from Meta Superintelligence Labs

Company says it has broken ground on 10 data centers in the last 24 months for AI-optimized capacity

Competitive Standing

Largest direct competitive position is in social attention and ad delivery

3.56 billion Family daily active people in March 2026 — among the largest user bases of any consumer platform

Owns several of the world’s largest consumer apps and ad-delivery systems

Position differs by rival

Alphabet leads search-intent and scaled video via YouTube; Amazon owns commerce-intent inventory near point of purchase

TikTok has a powerful short-video recommendation engine and large attention share with younger users

Snap holds AR-oriented positioning with younger audiences; Pinterest holds explicit commercial-intent discovery

Direction of advantage looks stable

Better: ad impressions and average price per ad both rose in Q1 2026; AI ranking and ad tools improving

Worse: Reality Labs remains loss-making, switching costs are limited, and US/EU regulatory pressure remains high

Competitive Advantage

Network effects: high

3.56 billion Family daily active people; users and advertisers reinforce each other across Facebook, Instagram, Messenger, WhatsApp, and Threads

Intangible assets: high

Owns several of the world’s largest consumer apps and ad-delivery systems; AI ranking and Advantage+ tools showed measurable conversion improvements

Barriers to entry: high

$131.05B of non-cancelable contractual commitments and large compliance burdens; 2026 capex guided $125–$145B

Cost advantage: medium

Scale benefits in ad inference, measurement, and infrastructure — partly offset by very large ongoing capex; switching costs are low for users and low-to-medium for advertisers

Upcoming Catalysts

Near-term reporting and corporate events

May 27, 2026 annual meeting

Q2 2026 revenue guided to $58B–$61B

Q1 2026: revenue $56.31B; ad impressions and average price per ad both rose

AI infrastructure build and product roadmap

2026 capex range raised to $125B–$145B (from $115B–$135B)

April 30, 2026: $25B of investment-grade bonds issued to fund AI infrastructure

Muse model family launched as first products from Meta Superintelligence Labs

Strong Financial Position

Balance sheet: medium gross leverage, low net leverage

March 31, 2026: $58.75B long-term debt; $81.18B cash, equivalents, and marketable securities

Net cash position before April 30 financing; $25B bond issuance subsequently raised gross debt with corresponding cash

Cash flow generation

Q1 2026 operating cash flow: $32.23B

Q1 2026 free cash flow: $12.39B (after $19.84B of capex)

Reinvestment intensity: high

FY2025 capex: $72.22B; 2026 capex guidance raised to $125B–$145B

Share repurchases and dividends continued alongside elevated AI and hardware investment

Why it trades at a deep discount

AI investments need to prove they will produce attractive returns

AI has already shown to improve advertising effectiveness

The plan for monetization is not totally laid out yet but there are some clear opportunities

Shopping in Facebook and Instagram has been successful and Meta AI has the possibility of enhancing that experience for users if it’s good (which Muse Spark has shown it is)

Competitors are pursuing similar strategies

“We’re already testing an early version of business AIs, and weekly conversations have grown 10x since the start of this year.” – Mark Zuckerberg, Q1 2026 earnings call

AI investments reduce income available to shareholders

Meta has historically had high ROIC (>30%)

Meta has high margins with a strong balance sheet, allowing for cheap financing of capital, reducing interest expenses

Being a tech company, they can fully leverage AI for productivity and efficiency gains to help offset capital expenditures (more regulated industries have to be careful)

Reality Labs has wide losses

While the Metaverse has failed, smart glasses have done extremely well

“Our AI glasses continue to perform well with the number of people using them daily tripling year-over-year.” – Mark Zuckerberg, Q1 2026 earnings call

You win some, you lose some

“We remain the biggest investor in the VR space across the industry, but we are focused on making our VR business sustainable as we invest more in other areas like AI and glasses.” – Mark Zuckerberg, Q1 2026 earnings call

Management has acknowledged it and is taking steps to correct it

Legal and Regulatory

Both voters and lawmakers have unfavorable views on social media

It is unlikely these issues are resolved in Meta’s favor, which warrants a discount to historical valuation

Management

Founder-led with deep ownership alignment

Mark Zuckerberg, founder, chairman, and CEO since 2004 (~22 years); controlled 60.8% of voting power as of April 1, 2026

$1 salary; does not participate in the annual cash bonus plan

Broader executive team

Subject to stock ownership guidelines, but the annual cash bonus framework is committee-discretionary and tied to broad priorities rather than explicit operational milestones

Capital allocation evidence

Willingness to fund operating priorities (capex rose from a 2023 plan of $34–39B to a 2026 plan of $125–145B); share repurchases and dividends continue alongside elevated investment

Product launches: largely on time Ray-Ban Stories (2021), Quest Pro (2022), Quest 3 (2023), Llama 2 (2023), Llama 3 / Meta AI (April 2024) all shipped within stated windows

2022–23 cost reset achieved

”Year of efficiency”: headcount down 22% year over year by Q4 2023; management stated efficiency goals were achieved middle-management layers were reduced, and management declared the initiative achieved by early 2024

The cost reset worked: later expense guidance declined and management explicitly cited the leaner org as enabling faster execution

Reels and ads rebuild delivered, but slowly

By Q2 2023, Reels run-rate exceeded $10B; Advantage+ end-to-end revenue more than doubled YoY by Q1 2024

Weaker areas

Budget discipline and long-cycle disclosure

2025 capex revised from $60–65B to $70–72B; 2026 capex revised from $115–135B to $125–145B within a quarter

Reality Labs unit economics and “most-used AI assistant” benchmark remain unverified

Management has shown they operate as owners and understand what drives business value.

Earnings Growth

Meta guided to Q2 2026 revenue of $58B–$61B on the Q1 2026 earnings call (April 29, 2026)

Revenue trajectory: $134.90B (2023, +16%), $164.50B (2024, +21%), $200.97B (2025, +22%); Q1 2026 $56.31B

Q1 2026 ad impressions and average price per ad both rose; AI-driven ad ranking and Advantage+ tools showed measurable conversion improvements

Industry: digital advertising remains the dominant pool, with consumer AI and VR/AR as adjacent growth vectors

3.56B Family DAP gives the largest reachable ad audience among scaled peers

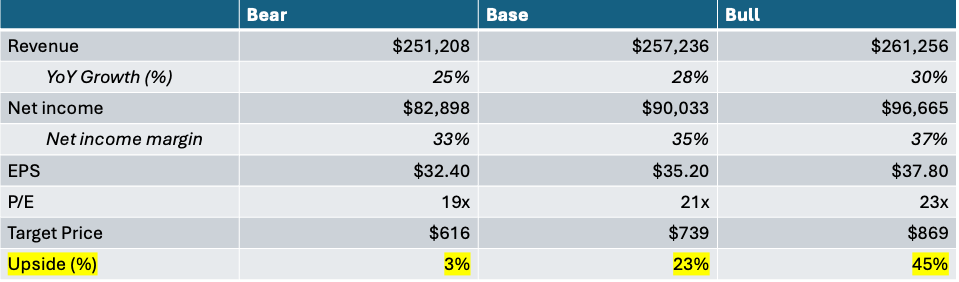

Valuation – 80% confidence range

Risks

Concentration in advertising

Substantially all revenue is from advertising on Facebook and Instagram; advertisers lack long-term commitment. Severity: Medium

Downturn in spending because of recession unlikely

AI has shown it works in advertising

Competition for users and ad budgets

TikTok and other platforms strong with younger users; Alphabet and Amazon contest large ad budgets. Severity: Medium

Regulatory, litigation, and antitrust exposure

EU/US matters across privacy, content, youth safety, AI, and competition could significantly affect results. Severity: Medium | Probability: High

Capital intensity and AI execution risk

2026 capex raised from $115–135B to $125–145B in one quarter; predictability has weakened. Severity: High

Meta Platforms: Summary Investment Thesis

Massive scale: 3.56B Family DAP and FY2025 revenue of $200.97B (+22% YoY)

Wide moat: high network effects, intangibles, and barriers to entry; advantage looks stable

Strong cash generation: Q1 2026 OCF $32.23B

High return on invested capital

Demonstrated operating discipline: 2023 ‘year of efficiency’ delivered

Meta smart glasses have been a huge success and provide another point of AI interaction

Have accepted Reality Labs shortcomings and taken steps to pivot

AI has proven to improve advertising + promising early signs from Muse Spark / Meta AI

Market is pricing in a bear scenario leaving asymmetric upside

Meta is a good business, in a good industry, with good management, at a good price.